White HouseSenateThe HouseSupreme CourtFederal ReserveDOJState DepartmentTreasuryCensusBudget OfficeTrade Representative

WashingTone

Informed by Washington, Defined by Insight

Wednesday, May 20, 2026

WashingTone

Rising Costs Put Affordable Care Act Coverage at Risk for Millions of Americans

Expiring subsidies and premium increases threaten to sharply reduce enrollment as policymakers clash over how to stabilize the US health insurance system

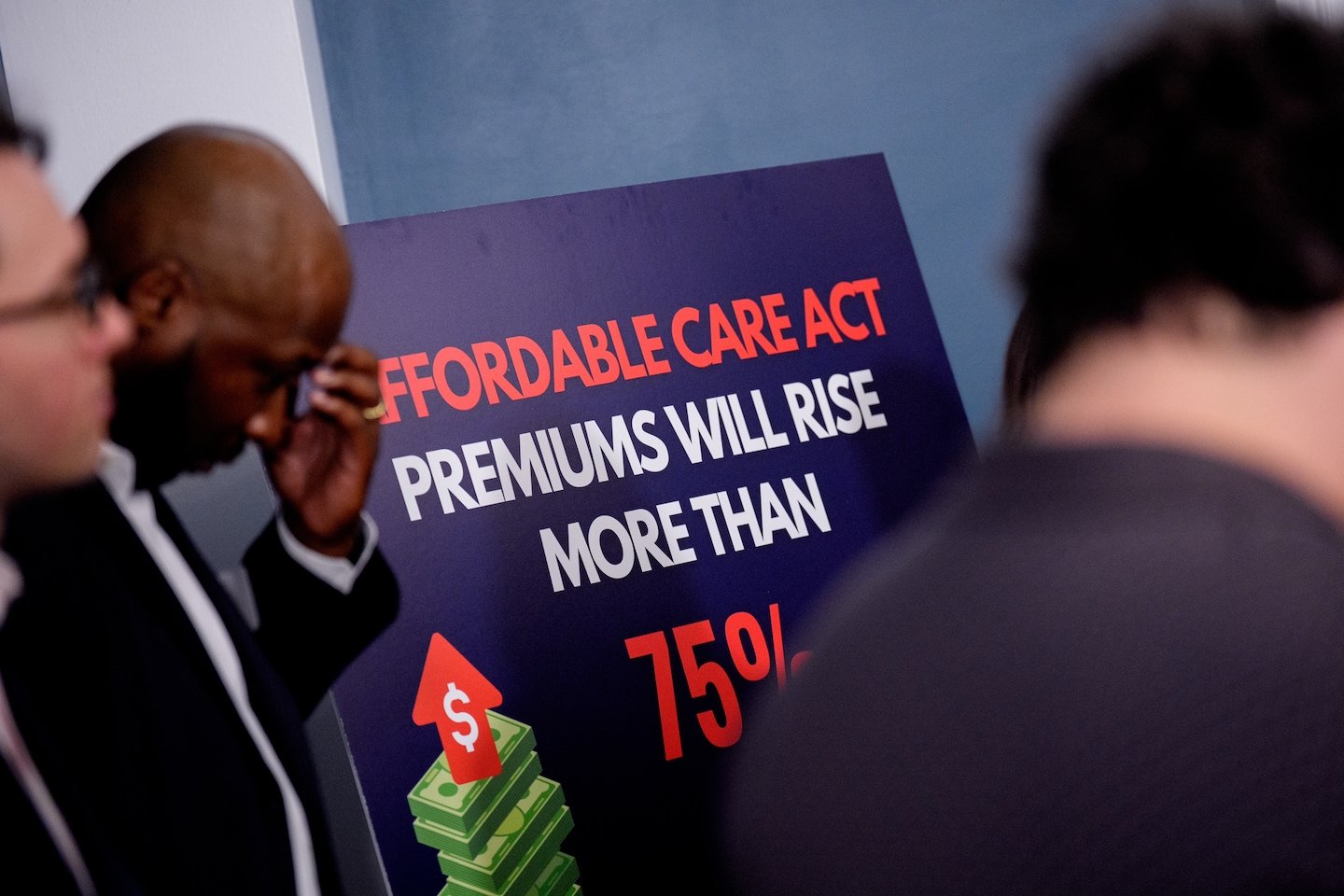

SYSTEM-DRIVEN pressure on the United States health insurance framework is intensifying as analysts and policymakers warn that millions of people could lose Affordable Care Act coverage if rising premiums and subsidy changes continue on their current trajectory.

The concern centers on how federal support mechanisms for marketplace insurance plans are structured and whether they will remain sufficient to keep coverage affordable for lower- and middle-income households.

The Affordable Care Act created subsidized insurance marketplaces designed to expand access to private health coverage for individuals without employer-based insurance.

These subsidies significantly reduce monthly premiums for eligible enrollees, making coverage financially viable for millions of Americans.

However, recent policy debates and scheduled adjustments to federal assistance levels have raised the prospect of higher out-of-pocket costs for many enrollees.

What is confirmed is that enrollment in ACA marketplaces has grown substantially in recent years, supported in part by expanded subsidy provisions introduced during pandemic-era policy interventions.

Those enhanced subsidies lowered premium costs and helped drive record participation.

The key concern now is what happens if those enhanced supports are reduced or allowed to expire, particularly in a context where underlying insurance premiums continue to rise due to broader health care cost inflation.

Health economists warn that even modest increases in monthly premiums can trigger significant coverage losses among individuals who are price-sensitive or living near eligibility thresholds for subsidies.

In the US system, insurance coverage is closely tied to employment status and income level, meaning changes in federal subsidy policy can quickly translate into shifts in the insured population.

Policy debate around the Affordable Care Act remains highly polarized.

Supporters argue that maintaining or expanding subsidies is necessary to preserve access and prevent a surge in the uninsured rate.

Opponents of expanded subsidies argue that the long-term cost to the federal budget is unsustainable and that market forces should play a larger role in determining premiums and enrollment levels.

The stakes are particularly high for working-class households and small business employees who do not receive employer-sponsored insurance and rely heavily on the marketplace.

Analysts caution that if affordability deteriorates, coverage losses could concentrate in precisely these groups, increasing pressure on emergency care systems and uncompensated hospital care.

State-level insurance regulators and health systems are also preparing for potential volatility in enrollment patterns, as shifts in federal policy often require rapid adjustments in outreach, pricing, and risk pooling.

Insurers participating in ACA marketplaces must also recalibrate premiums based on expected changes in enrollment composition, which can further amplify cost fluctuations.

The trajectory of coverage in the coming period will depend heavily on federal legislative decisions regarding subsidy extensions and broader health financing policy.

The outcome will directly determine whether the Affordable Care Act continues to expand coverage gains or enters a phase of significant enrollment contraction driven by affordability pressures.

The concern centers on how federal support mechanisms for marketplace insurance plans are structured and whether they will remain sufficient to keep coverage affordable for lower- and middle-income households.

The Affordable Care Act created subsidized insurance marketplaces designed to expand access to private health coverage for individuals without employer-based insurance.

These subsidies significantly reduce monthly premiums for eligible enrollees, making coverage financially viable for millions of Americans.

However, recent policy debates and scheduled adjustments to federal assistance levels have raised the prospect of higher out-of-pocket costs for many enrollees.

What is confirmed is that enrollment in ACA marketplaces has grown substantially in recent years, supported in part by expanded subsidy provisions introduced during pandemic-era policy interventions.

Those enhanced subsidies lowered premium costs and helped drive record participation.

The key concern now is what happens if those enhanced supports are reduced or allowed to expire, particularly in a context where underlying insurance premiums continue to rise due to broader health care cost inflation.

Health economists warn that even modest increases in monthly premiums can trigger significant coverage losses among individuals who are price-sensitive or living near eligibility thresholds for subsidies.

In the US system, insurance coverage is closely tied to employment status and income level, meaning changes in federal subsidy policy can quickly translate into shifts in the insured population.

Policy debate around the Affordable Care Act remains highly polarized.

Supporters argue that maintaining or expanding subsidies is necessary to preserve access and prevent a surge in the uninsured rate.

Opponents of expanded subsidies argue that the long-term cost to the federal budget is unsustainable and that market forces should play a larger role in determining premiums and enrollment levels.

The stakes are particularly high for working-class households and small business employees who do not receive employer-sponsored insurance and rely heavily on the marketplace.

Analysts caution that if affordability deteriorates, coverage losses could concentrate in precisely these groups, increasing pressure on emergency care systems and uncompensated hospital care.

State-level insurance regulators and health systems are also preparing for potential volatility in enrollment patterns, as shifts in federal policy often require rapid adjustments in outreach, pricing, and risk pooling.

Insurers participating in ACA marketplaces must also recalibrate premiums based on expected changes in enrollment composition, which can further amplify cost fluctuations.

The trajectory of coverage in the coming period will depend heavily on federal legislative decisions regarding subsidy extensions and broader health financing policy.

The outcome will directly determine whether the Affordable Care Act continues to expand coverage gains or enters a phase of significant enrollment contraction driven by affordability pressures.