White HouseSenateThe HouseSupreme CourtFederal ReserveDOJState DepartmentTreasuryCensusBudget OfficeTrade Representative

WashingTone

Informed by Washington, Defined by Insight

Tuesday, May 19, 2026

WashingTone

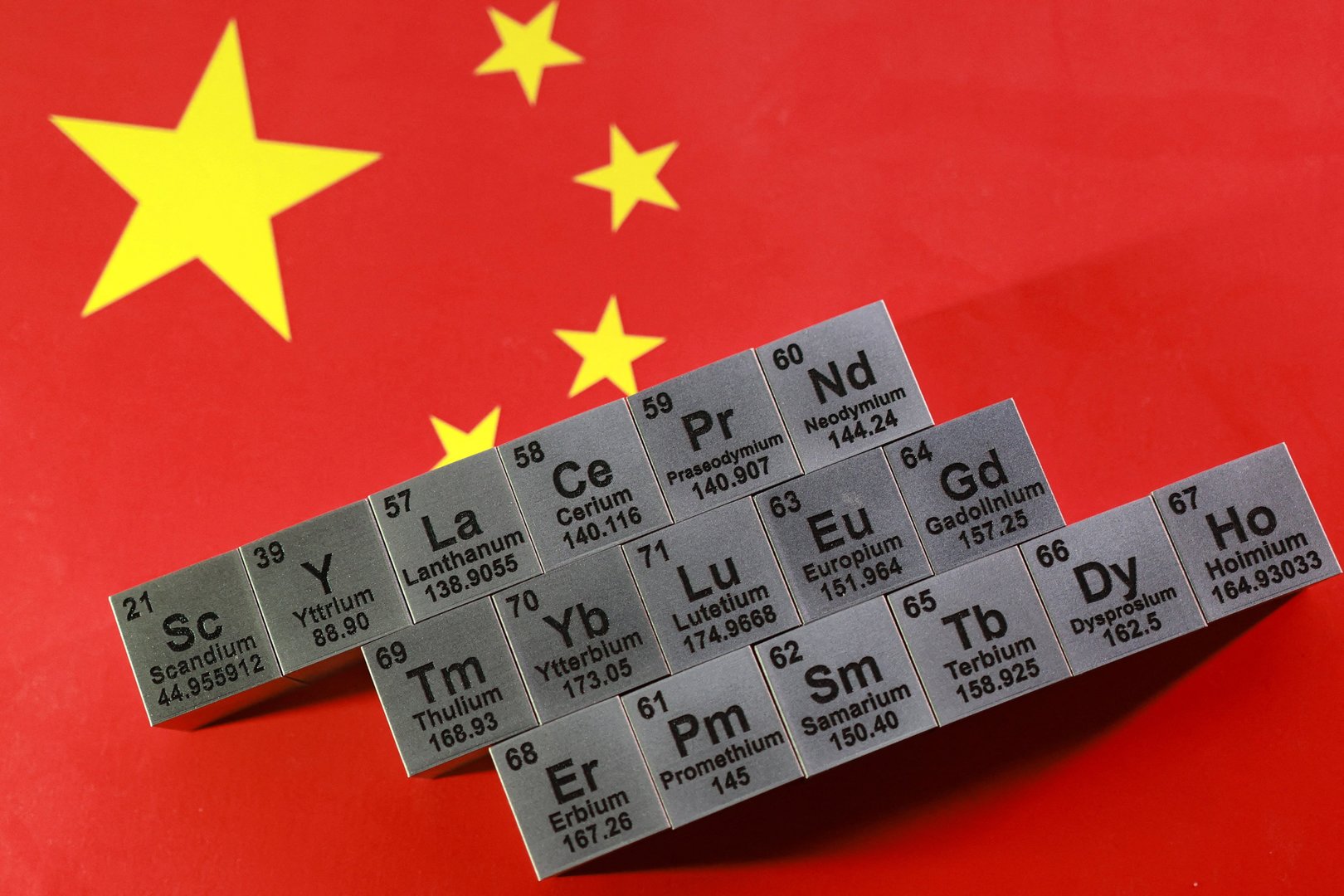

U.S. Secures Limited Rare Earth Relief as China Keeps Tight Grip on Export System

A narrow easing in access to critical minerals offers Washington short-term relief, but Beijing’s licensing framework continues to define global rare earth supply chains.

SYSTEM-DRIVEN: The story is driven by the structure of global critical mineral supply chains and the policy framework governing rare earth exports from China, which remains the dominant force shaping availability and pricing worldwide.

The United States has obtained a limited improvement in access to rare earth materials used in advanced manufacturing, defense systems, and clean energy technologies, but the underlying export control system operated by China remains fully in place and continues to shape global supply conditions.

What is confirmed is that rare earth elements are not scarce in the earth’s crust, but their processing and refining are heavily concentrated in China, which has built a tightly regulated export licensing regime over several years.

This system allows Beijing to control the flow of processed materials that are essential for magnets, semiconductors, electric vehicle motors, and military-grade components.

The latest development reflects a constrained easing rather than a structural shift.

The United States has gained some incremental access through limited commercial arrangements and selective approvals, but these do not alter the broader architecture of China’s export controls, which remain the central mechanism governing outbound shipments of refined rare earth products.

The key issue is that even small changes in approval rates or licensing terms can have outsized effects on downstream industries.

Rare earth supply chains operate with narrow margins for substitution, meaning that short-term relief for one category of material does not necessarily translate into broader stability for manufacturers.

China’s export regime continues to function as a policy tool that balances domestic industrial priorities with external trade relationships.

The licensing system allows authorities to regulate volume, destination, and timing of shipments, giving Beijing significant leverage over global industries that depend on these inputs.

For the United States, the limited gain underscores a structural vulnerability that remains unresolved.

Domestic production of rare earth processing capacity is expanding but still accounts for a small share of global refining output.

As a result, even modest disruptions or policy adjustments abroad can influence supply availability and pricing in U.S. markets.

The defense sector is particularly exposed, as rare earth materials are used in precision-guided systems, radar technologies, and advanced electronics.

Industrial manufacturers face similar constraints, especially in electric vehicle and renewable energy supply chains where high-performance magnets are essential.

While the recent easing is viewed as a short-term improvement in access conditions, it does not represent a policy reversal by China.

The export regime remains intact, and its core function—centralized control over refined rare earth flows—continues to define the global market structure.

The broader trajectory is one of continued strategic competition over critical minerals, where incremental shifts in licensing or trade arrangements provide temporary relief but do not alter the underlying dependency dynamics that both sides are actively trying to reshape.

The United States has obtained a limited improvement in access to rare earth materials used in advanced manufacturing, defense systems, and clean energy technologies, but the underlying export control system operated by China remains fully in place and continues to shape global supply conditions.

What is confirmed is that rare earth elements are not scarce in the earth’s crust, but their processing and refining are heavily concentrated in China, which has built a tightly regulated export licensing regime over several years.

This system allows Beijing to control the flow of processed materials that are essential for magnets, semiconductors, electric vehicle motors, and military-grade components.

The latest development reflects a constrained easing rather than a structural shift.

The United States has gained some incremental access through limited commercial arrangements and selective approvals, but these do not alter the broader architecture of China’s export controls, which remain the central mechanism governing outbound shipments of refined rare earth products.

The key issue is that even small changes in approval rates or licensing terms can have outsized effects on downstream industries.

Rare earth supply chains operate with narrow margins for substitution, meaning that short-term relief for one category of material does not necessarily translate into broader stability for manufacturers.

China’s export regime continues to function as a policy tool that balances domestic industrial priorities with external trade relationships.

The licensing system allows authorities to regulate volume, destination, and timing of shipments, giving Beijing significant leverage over global industries that depend on these inputs.

For the United States, the limited gain underscores a structural vulnerability that remains unresolved.

Domestic production of rare earth processing capacity is expanding but still accounts for a small share of global refining output.

As a result, even modest disruptions or policy adjustments abroad can influence supply availability and pricing in U.S. markets.

The defense sector is particularly exposed, as rare earth materials are used in precision-guided systems, radar technologies, and advanced electronics.

Industrial manufacturers face similar constraints, especially in electric vehicle and renewable energy supply chains where high-performance magnets are essential.

While the recent easing is viewed as a short-term improvement in access conditions, it does not represent a policy reversal by China.

The export regime remains intact, and its core function—centralized control over refined rare earth flows—continues to define the global market structure.

The broader trajectory is one of continued strategic competition over critical minerals, where incremental shifts in licensing or trade arrangements provide temporary relief but do not alter the underlying dependency dynamics that both sides are actively trying to reshape.